China’s Power Battery Participates in Global Lithium Battery Competition

I. Lithium battery battlefield shift: from capacity involution to global layout

1. China’s lithium battery cluster strategy in Southeast Asia

Malaysia’s lithium battery industry chain closed loop:

- LiWei Lithium Energy: 680 million cylindrical batteries have been mass-produced + 8.654 billion yuan energy storage battery project (Kedah);

- Material supporting: 2 billion square meters of diaphragm of Xingyuan Material, 90,000 tons of cathode materials of Hunan Yuneng, 50,000 tons of anode materials of Shangtai Science and Technology;

- Terminal application: Zero Run Auto and Stellantis cooperated with the localization of assembling the C10 model (the end of 2025) Cost and Tariff Advantage: Malaysia’s comprehensive cost)

Cost and tariff advantage:

- Malaysia’s comprehensive cost is 15%-25% lower than China’s (land/energy/labor+tax incentives);

- Tariffs to the U.S. have been reduced from 25% to 19%, avoiding the risk of China’s high tariffs on batteries at 173%.

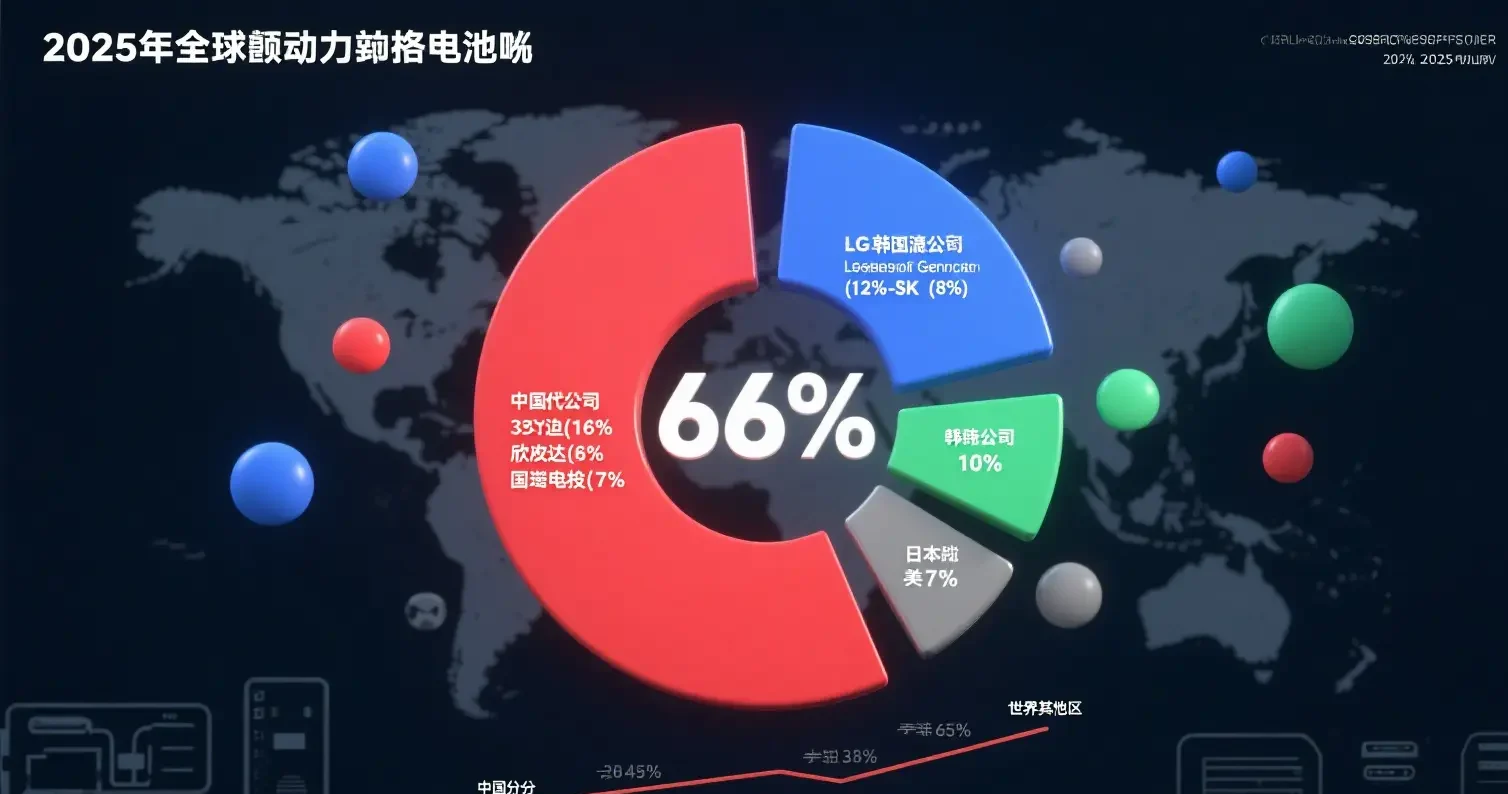

2. Global production capacity share is solid

Global power battery installed capacity of 465.9GWh in the first half of 2025, with China accounting for 61.8% (288.1GWh) and the U.S. only 12.4% (57.6GWh).3 China’s speed of technology iteration (e.g., CTP/sodium power) and scale advantage are still core competitiveness.

Engineer insight: Southeast Asia cluster is not “capacity relocation”, but the supply chain toughness upgrade – materials – core – vehicle closed loop replica to the tariff safety zone.

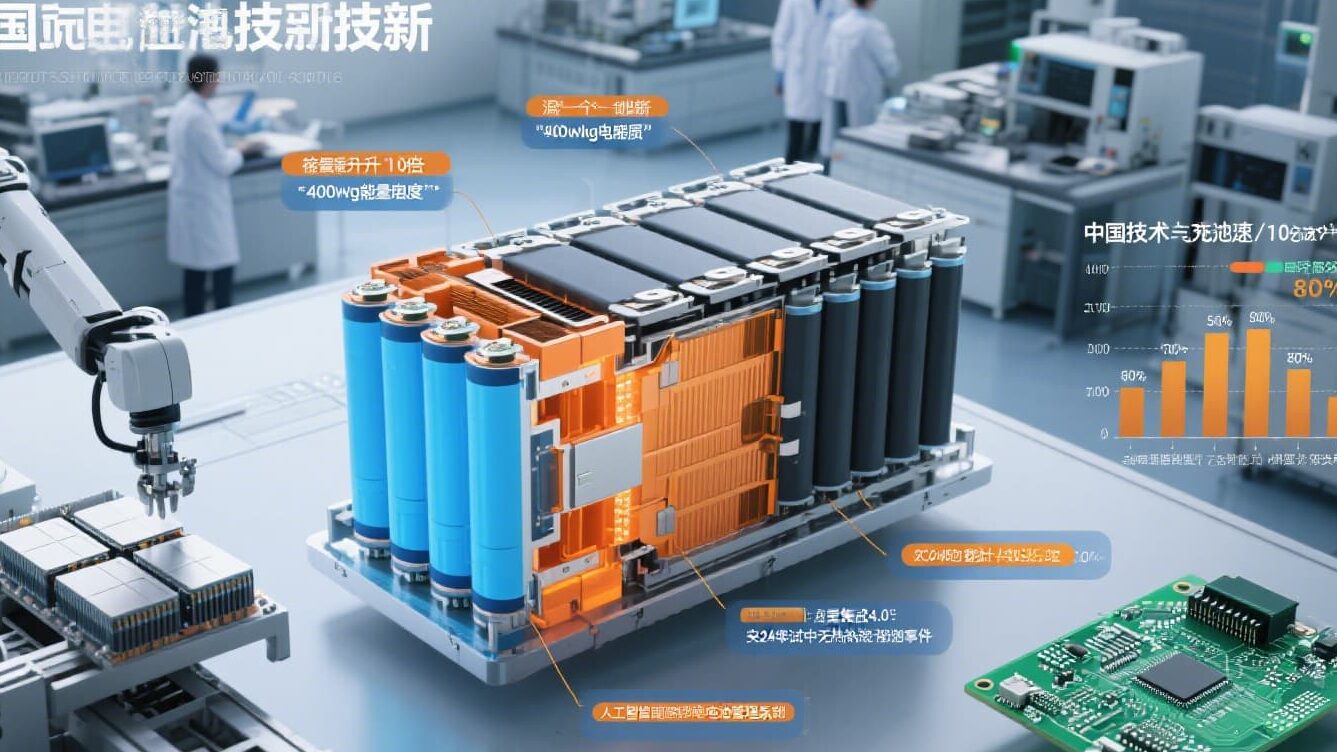

II, lithium battery technology counterattack: lithium iron phosphate breakthroughs in Europe and the United States enterprises and patent encirclement

1. Lithium iron phosphate (LFP) technology proliferation

LG New Energy’s transformation:

- won Tesla’s $4.3 billion energy storage order (39GWh/3 years), adopting CTP+soft pack core solution, energy density increased by 5%;

- Poland/Michigan factory exclusively for LFP, to circumvent the localization restrictions of the Inflation Reduction Act.

The essence of technology gap:

- LFP has no technical barriers due to its intrinsic safety advantage (stable structure of iron phosphorus-oxygen tetrahedra), while Chinese enterprises have advantages in process precision (yield >95%) and cost control ($80/kWh).

2. Patent War: Tulip Alliance’s Sniping Logic

Patent pool operation mechanism:

- LG New Energy and Panasonic hold 1500 patents, covering electrode preparation, electrolyte formulation and other basic processes;

- Focus of the litigation: 28 core patents on high-speed stacking process, silicon and carbon negative electrode interface treatment.

China’s path to break through:

- Invalidation: Hunan Yuneng applied for nano-coated lithium manganese iron phosphate patent (CN202410876XXX) in Europe, breaking through the traditional LFP crystal structure limitations;

- Cross-licensing: NDT and Bosch reached a patent swap of BMS algorithm in exchange for a European market pass.

III. China’s lithium breakthrough strategy: from technology upgrading to global collaboration

1. Anti-Involution: Capacity Optimization and Technology Deep Dive

Production capacity elimination:

- eliminate <1GWh inefficient production capacity and shift to sodium/solid state battery pilot line (e.g. Ningde Times cohesive battery pilot);

Material innovation:

- Li-rich manganese-based anode (specific capacity >280mAh/g) replaces high-voltage ternary to avoid the risk of nickel and cobalt resources.

2. Patent ecological reconstruction

| hierarchy | action plan | case |

|---|---|---|

| Defense layer | Formation of a lithium battery patent alliance | BYD/Zhongxin Innovation shares blade battery structure patent |

| Offensive layer | Layout New battery basic patents | Honeycomb Energy Sulfide All-Solid-State Electrolyte Patent (WO202512XXX) |

| arbitration layer | Promoting mutual recognition of standards between China and Europe | Negotiations for mutual recognition between GB 44240 and IEC 62619 are underway. |

3. Globalization 2.0: Technology Export and Localization Integration

- Europe: introduction of magnetron sputtering solid-state film process at Ningde Times’ German plant, adapted to BMW’s NEUE KLASSE platform;

- Latin America: BYD’s prioritization of PHEVs in Brazil (64% share), adapted to ethanol fueling infrastructure .

Conclusion: Main battlefield winners and losers – technology generation gap and supply chain power.

1. Short-term tug-of-war:

Southeast Asian clusters hedge against tariff risk; China’s overseas Li-ion production capacity will reach 380GWh in 2026 (accounting for 35% of the world);

2. Long-term battle:

- Europe and the US are holding on to the high-end market with patent barriers (e.g. automotive-grade NCM811);

- China needs to build up a generational advantage in solid-state batteries (sulfide electrolytes) and sodium batteries (layered oxide cathode).

3. Engineer’s declaration:

production capacity can be transferred, technology leadership can not be replicated – when China’s lithium-ion power from the “cost definer” to “standard setter”, the global competition rules will be reconstructed.